There are already many use cases for integrating wearable technology into life insurance.

Wearables are shown to provide a potential evidence source to inform an underwriting decision, increase customer engagement, and even improve consumer health and wellbeing. Wearable device metrics, if provided to insurance wellness programs, could potentially increase the insurability of people struggling with chronic conditions, provide a signal to insurers of healthy insureds, and improve the longevity of insurance customers. For insurers to effectively utilize wearable technology, it is important to understand the metrics captured by devices. A developing body of research evidence supports the relationship between these metrics and mortality. Taken together, this research could support a discount on life insurance premium due to reduced mortality expectations for people who demonstrate activity, adequate sleep levels, and healthy heart function.

Additional metrics available from wearables, such as more advanced heart capability evaluation as well as smoking indication, also show promise to impact mortality expectations. These developing areas require research as well as continued monitoring of technical developments to understand and assess their impact on mortality.

There is tremendous potential to incorporate wearable data into insurance product design and wellness program development. The wearable technology marketplace is continuing to expand. As device adoption rates increase and capabilities improve, potential insurance applications are also likely to grow. Insurers must, however, be mindful of regulations, set reasonable expectations, and balance the risk and rewards of new developments.

The Case for Wearable Technology in Life Insurance

Wearable technology has several different applications for the life insurance industry, including improved underwriting capabilities, value-added services for customers beyond insurance protection, and the potential to improve user health and well-being.

Fitness tracking devices gather health-related metrics that have the potential to generate insights about the user’s mortality and morbidity risk. Insurers are assessing if these metrics can be combined with data from other sources to yield faster underwriting decisions that are less invasive to the consumer than traditional underwriting methods. As wearable technology improves and devices become capable of gathering more sophisticated health-related information, it becomes more likely that insurers may be able to use wearable data to inform life insurance underwriting.

Insurance customers sometimes struggle to recognize the value of a product that provides protection over many years. Digital consumers, meanwhile, increasingly expect immediate benefits and ascribe value to experiential purchases. This shift in consumer preferences challenges insurers to remain relevant when the product being sold is both intangible and long-term. These devices can enable insurers to share health-related insights to consumers to help improve their health and well-being and provide additional value to the consumer beyond insurance protection. Additionally, these devices can reframe the relationship as a consumer-focused partnership.

Life insurance wellness programs are intended to encourage healthy behavior and improve both the quality and quantity of life of the participants. The World Health Organization estimates that 40 million people die each year from non-communicable diseases such as cardiovascular disease, cancer, respiratory diseases, and diabetes. Many of these deaths are related to lifestyle behaviors such as smoking, alcohol abuse, diet and physical inactivity.1 Wellness programs typically employ a wearable device to verify user activity and encourage users to make healthy lifestyle choices.

Consumers are increasingly using digital technology to research and purchase products online. These consumers expect the ability to purchase personalized products on demand. Wearable device capabilities enable insurance product offerings that meet these and other expectations of digital consumers.

Wearable Technology Marketplace

Wearables users are, for the most part, young: nearly half are between ages 18 and 34. Fitness trackers appeal to both men and women, and device owners are typically in higher income brackets, with one-third from households earning more than $100,000 per year.2, 3 The demographic makeup of wearable device users may be important for insurers to consider as they develop wearable-based wellness programs.

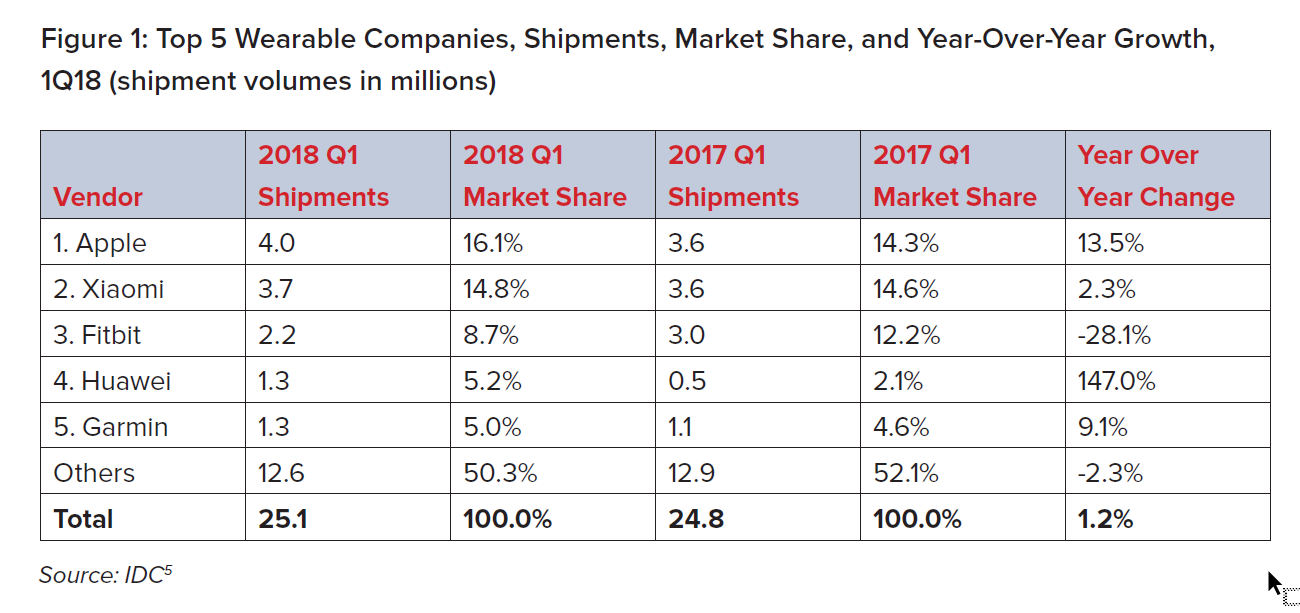

According to the 2017 Global Mobile Consumer Survey: US Edition, conducted by Deloitte, 23% of survey respondents owned a wearable fitness device and 13% owned a smartwatch.4 Wearable device shipments rose in 2018, with 25.1 million devices shipped in the first quarter alone, representing a 1.2% increase from the prior year.5 In 2017, the global market intelligence firm International Data Corporation (IDC) projected the wearable device market would double by 2021.6 However, it is worth noting that growth in device sales has slowed in 2018 relative to previous years.

The wearable device marketplace is also changing rapidly. Smartwatch sales are increasing: the release of new generations of the Apple Watch with improved capabilities and cellular connectivity has enabled Apple to become the leader in the wearable device marketplace. On the other hand, Fitbit and Garmin sales have declined, and Jawbone, one of the earliest wearable device maker leaders, went out of business in 2017. Also, although Fitbit continues to launch new products, it is no longer the number one fitness device maker.5

The top five wearable device make up less than half of the overall market. The market

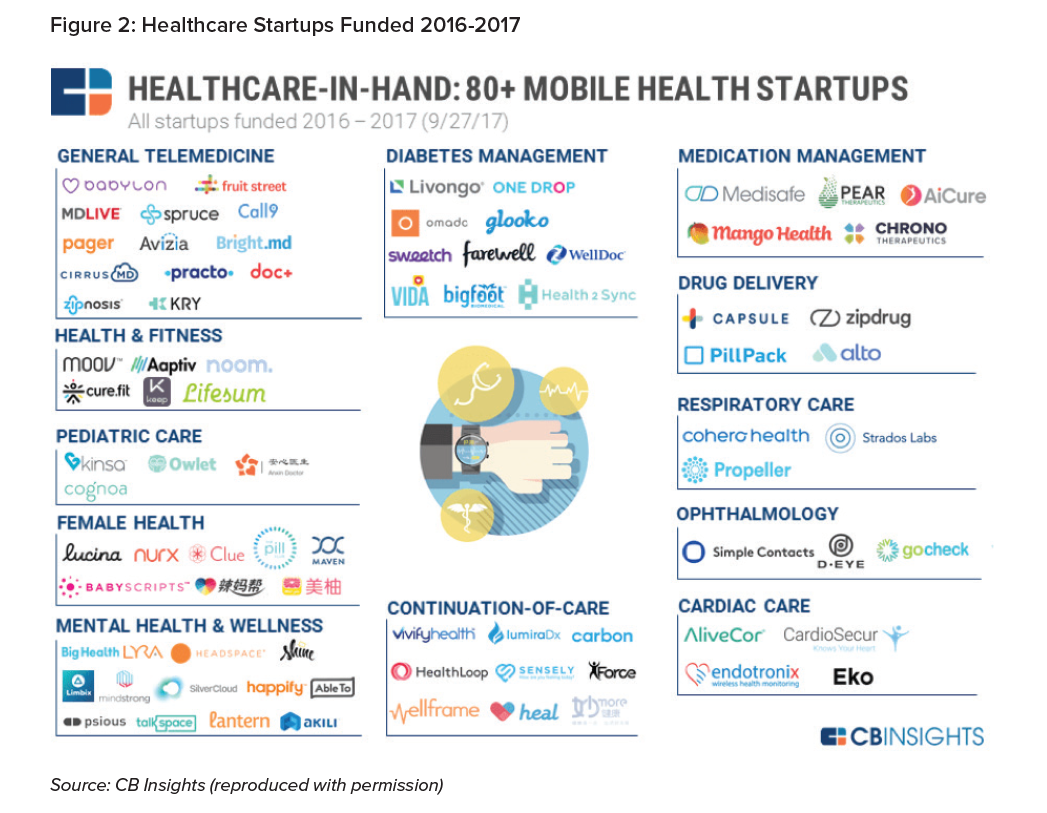

intelligence firm CB Insights currently tracks more than 300 companies operating in the wearable computing marketplace, a broadly defined cohort that consists of several categories, including health and fitness bands, smartwatches, virtual reality headsets, smart clothing, and biometric sensors (see Figure 2).

Health monitoring devices are continuing to develop beyond wearable fitness trackers. Medical technology startups are expanding their focus to address tracking metrics for specific conditions such as diabetes, respiratory care, and cardiac and mental health in addition to overall wellness, fitness and activity.

The rapidly changing device market presents a challenge for conducting research. For example, a study focused on the accuracy of a device might become obsolete before publication, as device makers are continuously rolling out improvements. There are also indications that metrics such as heart rate, commonly produced by wearable devices, vary in accuracy by device. A study of heart rate accuracy of seven wrist-worn wearable devices found that device accuracy varied by device as well as by activity. Overall, the study found, the devices were most accurate when measuring heart rate while cycling and least accurate when walking. Additionally, the study found that the Apple Watch produced the fewest errors in heart rate estimation.7

While it is necessary to assess the capabilities of devices currently in the market in order to evaluate the feasibility of implementing this technology in the insurance industry, a detailed review of device accuracy is beyond the scope of this paper.

Life Insurance Wellness Use Cases

One goal of life insurance wellness programs is to improve mortality and morbidity experience and is often enabled through data gathered from wearable devices. Wellness programs can provide consumer value through improved health, lower-priced insurance coverage, and increased insurability for consumers who might not otherwise have qualified for traditional coverage. Insurers, meanwhile, hope to benefit from lower claims experience resulting from improved mortality experience, increased sales, and improved customer engagement that could potentially lead to lower lapse rates.

Of course, the benefits of a wellness program depend on the health and activity level of program participants and their impact on the use cases of the program.

Wearable devices have several insurance applications for the chronically ill. Device data may support a decision not to write a policy or demonstrate active control of a chronic condition, improving the insurability of a person who might otherwise struggle to obtain coverage. Additionally, to the extent a chronic condition can be improved through healthy living, a wearable device used as part of a wellness program could improve the mortality expectation of chronically ill people as well as help prevent people with initial indications of certain chronic illnesses from developing those diseases.

Additionally, as people age, they tend to become heavier and many struggle to maintain their health. Wellness programs can benefit insurers by helping in-force policyholders improve their health, thereby improving in-force experience. Additionally, prospective consumers who aspire to improve their health could benefit from dynamic underwriting verified by wearable technology.

Wellness programs can also serve as a signal of the fit and healthy. Life insurance wellness programs typically offer rewards such as lower premiums and gift cards as well as discounts on consumer goods. The benefits associated with these policies should appeal to consumers who already participate in healthy activities.

Wellness programs with activity verified through a wearable device share some similarities with auto insurer usage-based insurance (UBI) programs, which assess and verify driving characteristics through telematics devices. UBI programs began in the U.S. in 2011 and are now offered by more than half of all U.S. auto insurers. These programs, which have experienced lower claim costs, are marketed to lower-mileage drivers, “safe” drivers (as assessed by specific driving behaviors), and younger drivers.8 Life insurers may expect improved claims experience from wellness programs designed to identify both health-conscious consumers and those whose behaviors distinguish their loss potential from others in their risk category who are not controlling their conditions.

Life Insurance-related wellness programs vary both in terms of rewards provided to incentivize behavior and, in the discounts, provided. Most of these programs use activity measurement, often including step counts, to track behaviors. Some life insurers also use resting heart rate and sleep metrics gathered from wearable devices to support a premium discount.

Wearable Device Metrics

Several studies have investigated the relationship between mortality risk and the metrics typically gathered from wearable devices. This paper provides examples of research support of several wearable device metrics but is not sufficient to support an actuarial pricing analysis of a wellness program discount. Such an analysis would need to include the full range of current literature and consider that many existing studies could benefit from more robust controls of variables that may be contributing to the mortality risk findings. Additionally, further analysis would need to combine several of these metrics in one multivariate study, rather than a single metric in isolation. Nevertheless, existing research can help insurers understand the ability of wearable devices metrics to differentiate all-cause mortality risk.

Steps

Dwyer, et al. (2015) investigated the link between average daily step counts and subsequent long-term all-cause mortality risk. The study, which followed approximately 2,500 Australian adults for about 10 years, found that a higher daily step count was associated with lower subsequent all-cause mortality. Specifically, the all-cause mortality hazard ratio was reduced by 6% for every 1,000 additional daily steps, adjusting for age, gender, body mass index (BMI), smoking status, alcohol consumption, and education level.9 It should be noted that the mortality benefit associated with steps presented in this research study may be higher than would be expected in an insured population. This is a single, relatively small study, and the

researchers did not control for all relevant variables, such as current health. However, this result provides support for using steps as a measure of activity in a life insurance wellness program due to the substantial association between step counts and all-cause mortality risk.

Physical activity

The U.S. Centers for Disease Control and Prevention (CDC) recommends weekly physical activity of:10

- At least 75 minutes of vigorous exercise,

- At least 150 minutes of moderate exercise, or

- Some equivalent combination of moderate and vigorous exercise per week.

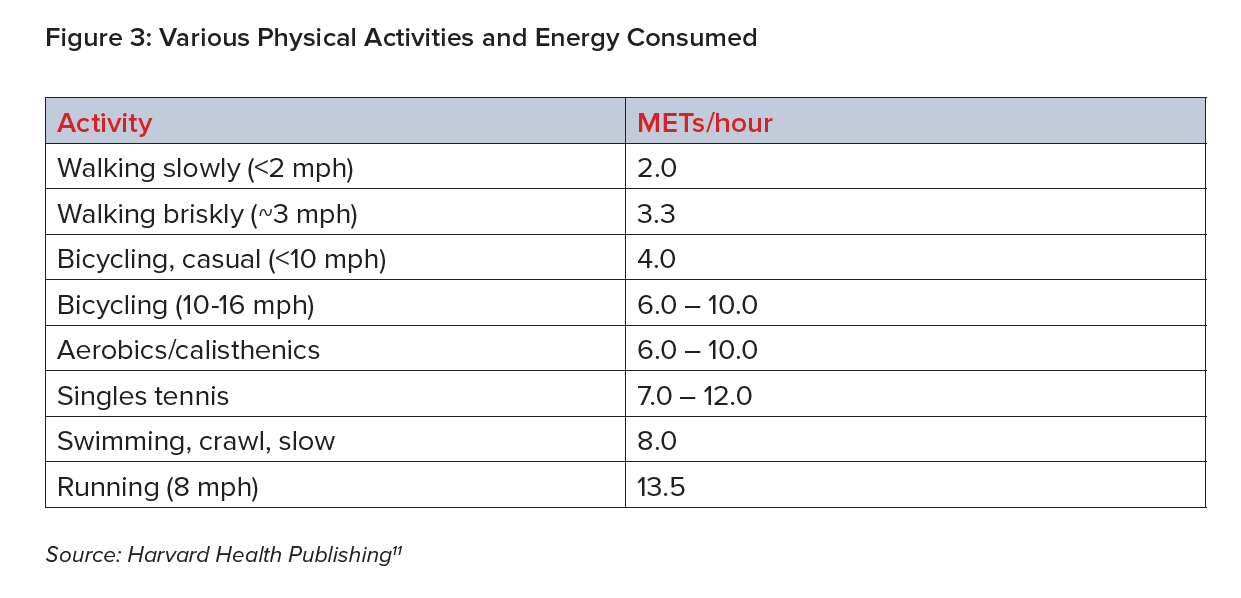

Researchers often measure physical activity in metabolic equivalents (METs) to compare various types of activity. Recommended physical activity guidelines can be expressed as engaging in at least 7.5 METs/hours per week. Examples of METs/hour for various activities include the following:11

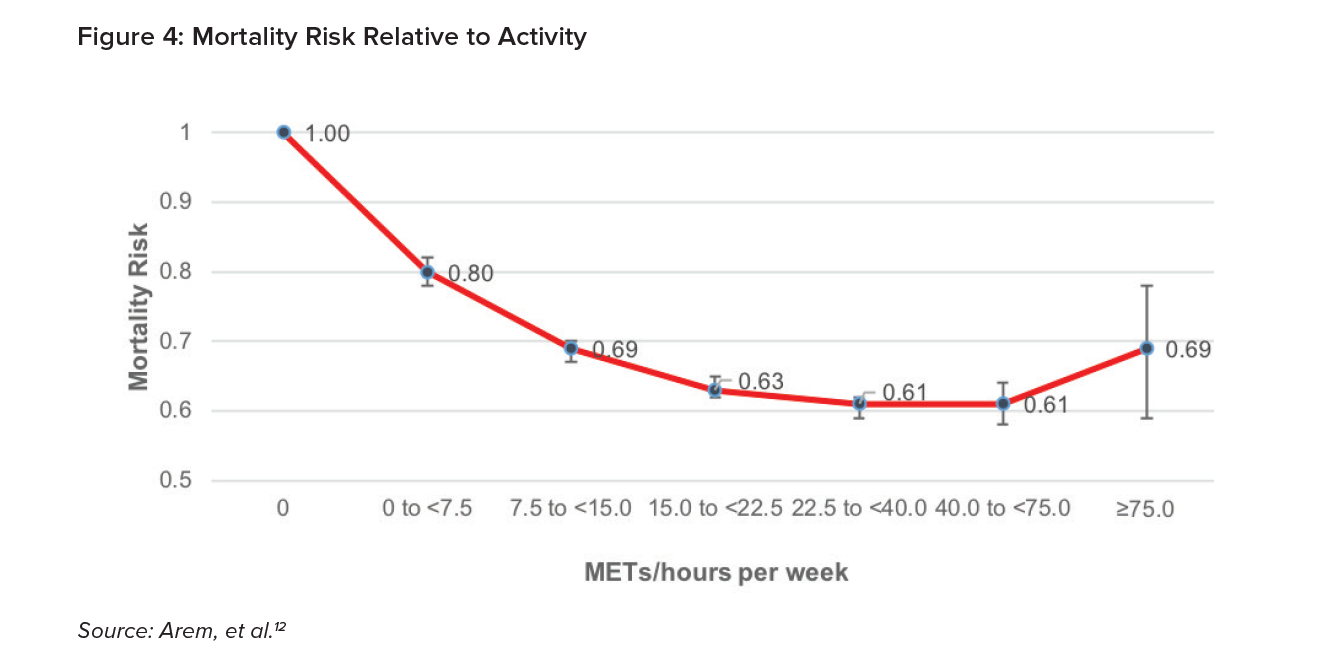

Arem, et al. (2015) examined the link between leisure time physical activity and mortality risk. This large, pooled study covered more than 600,000 men and women and more than 100,000 deaths. Risk was assessed using a Cox proportional hazards model after adjusting for age, sex, education level, smoking status, cancer history, heart disease, alcohol consumption, marital status and BMI. The following chart shows mortality risk at different levels of active hour per week, relative to inactivity.12

Their research indicates that even less physical activity than 7.5 METs/hours per week reduces mortality risk by 20% relative to no activity. At activity levels equivalent to one to two times higher than the recommended guidelines, the reduction in mortality risk is 31%. The lowest mortality risk is achieved when a person exercises three to five times more than the recommended activity guidelines.

This research demonstrates that physical activity is a metric that has a substantial association with improved all-cause mortality risk.

It may be important to note that this study does not control for the number of steps people take throughout the day. However, Dwyer, et al. (2015) found a relatively low correlation between daily step count and physical activity time. In a model that included daily step count and whether or not someone exercised vigorously for three or more hours each week, these researchers found both variables to be independently protective against mortality.

Inactivity

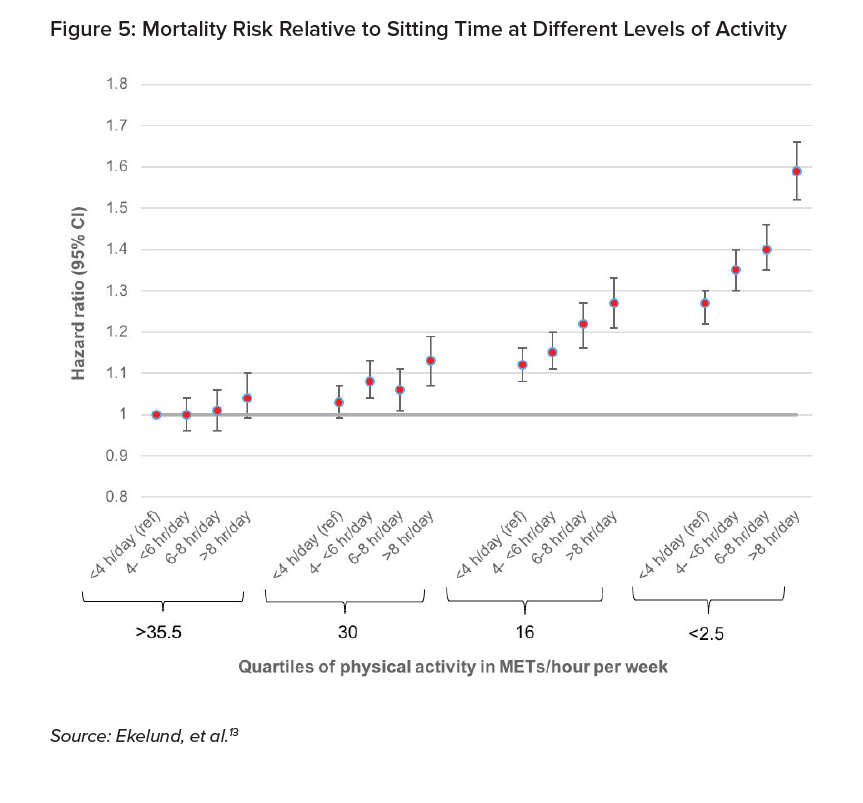

The link between physical inactivity and all-cause mortality was investigated by Ekelund, et al. (2016) in a large meta-analysis that included more than one million individuals and almost 85,000 deaths. Inactivity was assessed by total time per day spent sitting. The analysis showed the relative mortality risk for individuals split according to their METs/hours per week quartile of physical activity and for different levels of total sitting time. The chart below shows the mortality risk of each group relative to the risk of the most active group with the shortest total sitting time.13

Figure 5 shows the increased mortality risk associated with an individual’s total sitting time. Each activity group exhibits higher mortality if its members sit more than eight hours each day. Further, this relationship is more pronounced for those with lower activity levels. The mortality increase from sitting more than eight hours each day compared to less than four hours each day is slightly greater for the most active group but is 20% higher for the least fit group.

Including inactivity as a wellness program metric requires further investigation. Areas that could provide meaningful insights might include studying sitting over intermittent time periods as well as controls for daily step counts.

Resting heart rate

The link between resting heart rate and all-cause mortality was investigated by Zhang, et al. (2015) in a large meta-analysis covering 1.2 million participants and just over 78,000 deaths.14

The researchers controlled for many variables within their model, including blood pressure, smoking, BMI, physical activity, diabetes, alcohol, and education. This study found that every 10 beat-per-minute incremental decline in resting heart rate reduced all-cause mortality risk by 4% to 9%.14

Sleep

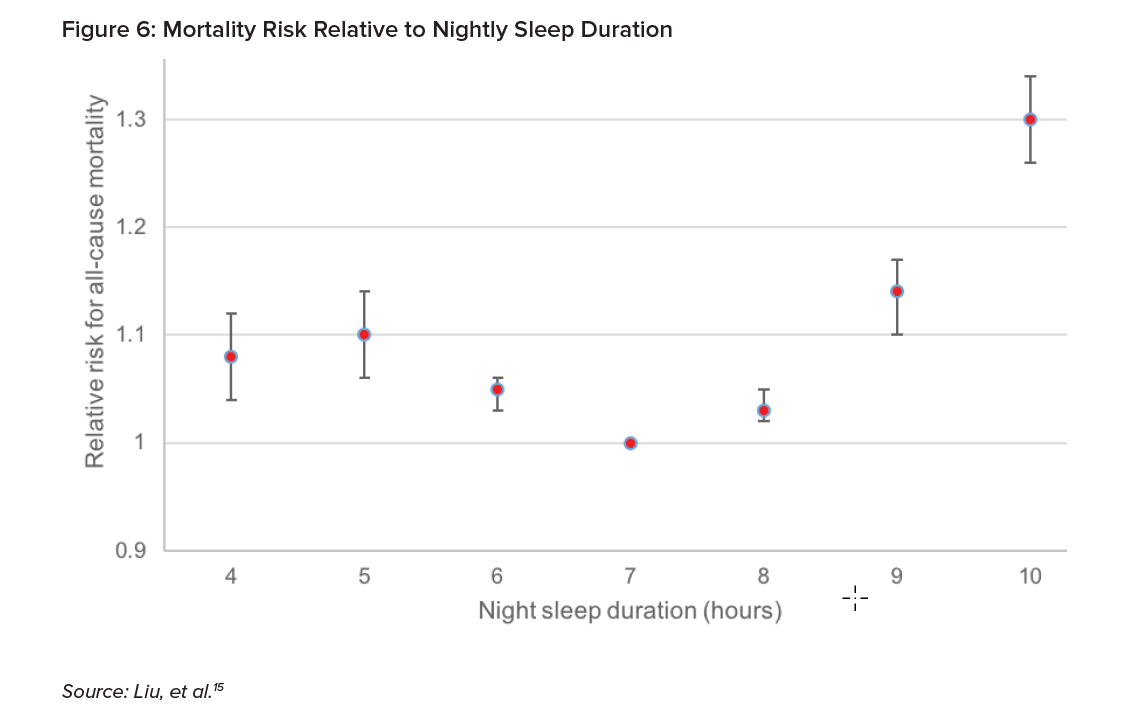

The link between sleep duration and all-cause mortality was investigated by Liu, et al. (2016) in another large meta-analysis covering 2.2 million individuals and 271,000 deaths. This paper presented the relative risk for all-cause mortality relative to night sleep for people under age 65. The chart shows that those sleeping seven hours a night had the lowest risk of all-cause mortality. At five hours a night, mortality risk increased by 10%; and interestingly, at nine hours a night, by 14%.15

There is some evidence that when people exercise, they report better sleep quality. However, it would not necessarily be expected that sleep duration would be highly correlated with other metrics that measure physical activity. Further research would be needed to confirm this assumption.

Emerging Metrics in Development

The wearable technology space is developing rapidly. Many new metrics are emerging that may have potential use in the insurance industry are currently captured on mainstream wearable devices. These metrics include heart rate measures beyond resting heart rate, stress level, body composition, and temperature.

VO2 Max

VO2 max represents the maximum volume (V) of oxygen (O2) that can be used by the body during exercise. It is the primary indicator of cardiorespiratory fitness, and insurers can use algorithms to estimate VO2 max from wearable data.

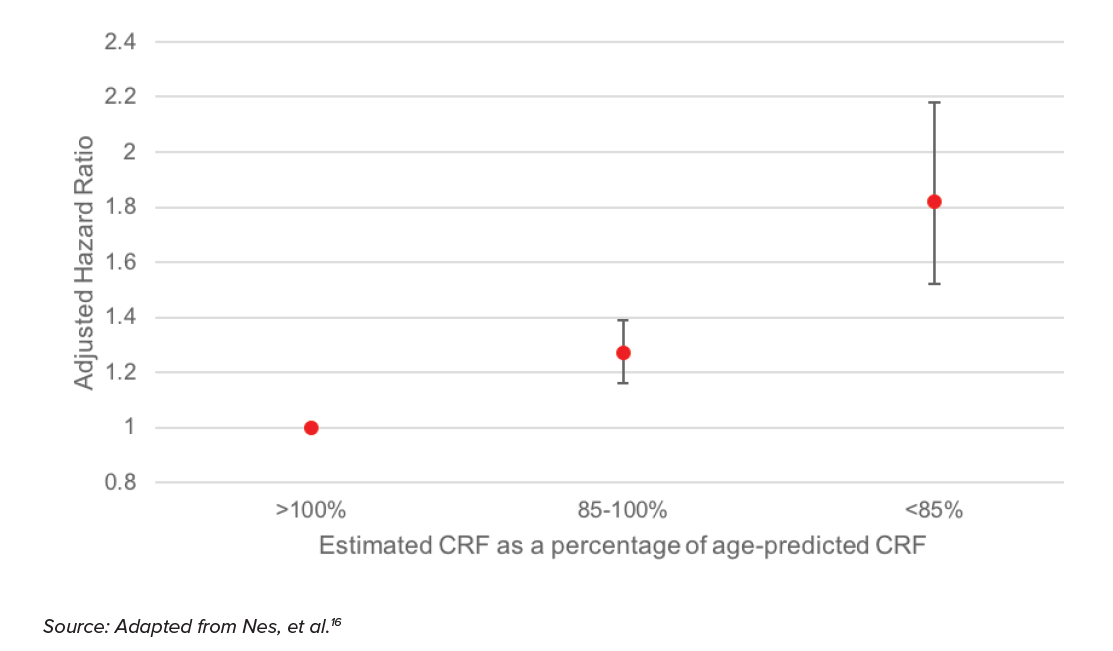

The link between cardiorespiratory fitness (CRF) and all-cause mortality risk was investigated by Nes, et al. (2014) in a study that compared actual against expected fitness levels based on age alone.16

The adjusted hazard ratio results are from a model that controlled for age, smoking, alcohol consumption, marital status, education, and family history of disease.

As shown in the chart above, a person with a fitness level of at least 15% below their age-predicted fitness level (<85% CRF) exhibits an 80% higher mortality risk (1.8 adjusted hazard ratio) compared to the baseline fitness level predicted by age alone. While the confidence interval is quite wide (ranging from around 1.5 to almost 2.2), even the low end of the interval exhibits a materially higher mortality risk than the baseline. This provides support for the assertion that cardiorespiratory fitness impacts mortality risk.

Pulse wave velocity

Every time the heart beats, it sends a pulse wave throughout the body. Pulse wave velocity measures how quickly this pulse wave travels through the circulatory system, and is linked to arterial stiffness, which is a precursor of cardiovascular disease. It measures oxygen levels in the blood and by extension the muscles and can indicate how the body is reacting to and recovering from aerobic training.

A meta-analysis by Vlachopoulos, et al. (2010) investigated the link between pulse wave velocity and all-cause mortality risk. It found that a one standard deviation increases in pulse wave velocity increased relative mortality risk by 42%.17 Pulse wave velocity is an emerging metric that may have the potential to differentiate mortality risk.

Detecting and monitoring illness

Wearable devices also have potential to provide early indication of certain illnesses and diseases. Atrial fibrillation, for example, is a condition where the heartbeat can become irregular and can be difficult to detect because the irregularities do not occur consistently. There would be significant potential benefit in wearing a device that monitors heart rate continuously throughout the day, as it would increase the possibility of identifying irregularities. The University of California, San Francisco's Health eHeart Study, which used the Apple Watch and its Cardiogram heart rate monitoring app, predicted heart irregularity with 97% accuracy.18

Wearable data can also provide early indication of certain illnesses before significant symptoms appear. For example, Li, et al. (2017) found that heart rate and body temperature variations outside of the normal range were associated with periods of inflammatory response.19 If this result could be replicated and developed successfully, it might be useful in monitoring higher-risk individuals and ensuring that treatments are provided as early as possible before complications develop.

Smoker identification

Some wearable devices are able to identify smoking behavior by identifying the signature movement of the hand bringing a cigarette to the mouth. This is far from a perfect solution. For example, it will not identify smoking behavior if someone holds a cigarette in their non-wearable hand. Additionally, the wearable might confuse smoking movements with the similar movement pattern of lifting a coffee cup to one’s mouth.

Future solutions to identify smoking without lab work will not solely rely on movement. It may be possible with a wearable device to identify some of the physiological changes to the body that happen as tobacco smoke is inhaled. Further, insurers interested in identifying applicants who are smokers could enhance the accuracy of smoker detection from wearable device data by combining the data with a predictive model designed to identify groups of likely smokers.

Wearable Data Considerations

While there is tremendous potential to include wearable data in life insurance products, there are some important considerations which can be described as the Four Rs of responsible data use:

- Regulations

- Reasonable expectations

- Risks

- Rewards

Regulations represent the minimum standard that must be achieved before using any new data source in insurance products. Regulatory guidance will likely include data protection and anti-discrimination considerations as well as local and regional regulatory focus. Many insurers are also acutely aware of the requirements of the European Union’s General Data Protection Regulation (GDPR) and the significant financial penalties for noncompliance.

Beyond regulatory concerns, insurers must also consider public perception. These may include expectations of fairness, trust and follow-through. Therefore, insurers must demonstrate transparency, employing effective communication that describes which data will be collected, how it will be protected, how it will be used, and just as importantly, how it will not be used.

There are also risks involved with relying on new data sources that extend beyond the risk of financial penalties. This includes risk of reputational damage beyond any individual insurance company to the insurance industry as a whole. Additionally, risks experienced by the wearable device industry could transfer to the insurance industry. These include class action lawsuits over accuracy, safety recalls, and privacy complaints.

Insurers must balance the potential risks with the rewards. Data from wearable devices hold the potential to help the insurance industry adapt to changing consumer expectations, enabling a quicker sale. Additionally, wearable devices that are part of an insurance company wellness program hold the potential to encourage active, healthy living, which benefits insurance company mortality experience as well as the well-being of insurance customers.

Conclusion

The market for wearable technology continues to grow and has many potential applications that could revolutionize the life insurance industry. Technological advances have the potential to improve overall health, expand insurability to people battling chronic conditions, and provide a signal to insurers of consumers who are fit and health conscious. There is certainly a relationship between physical activity and overall health.

As insurers consider how to include wearable device data in insurance products, it is imperative to understand the relationship between the metrics captured from wearable devices and mortality. Insurers must understand the metrics from wearable devices in order to effectively quantify the impact on health. It is the responsibility of insurers to understand the impact of wearables on mortality in order to communicate effectively with regulators and respond to the evolving marketplace.